{kind=link}

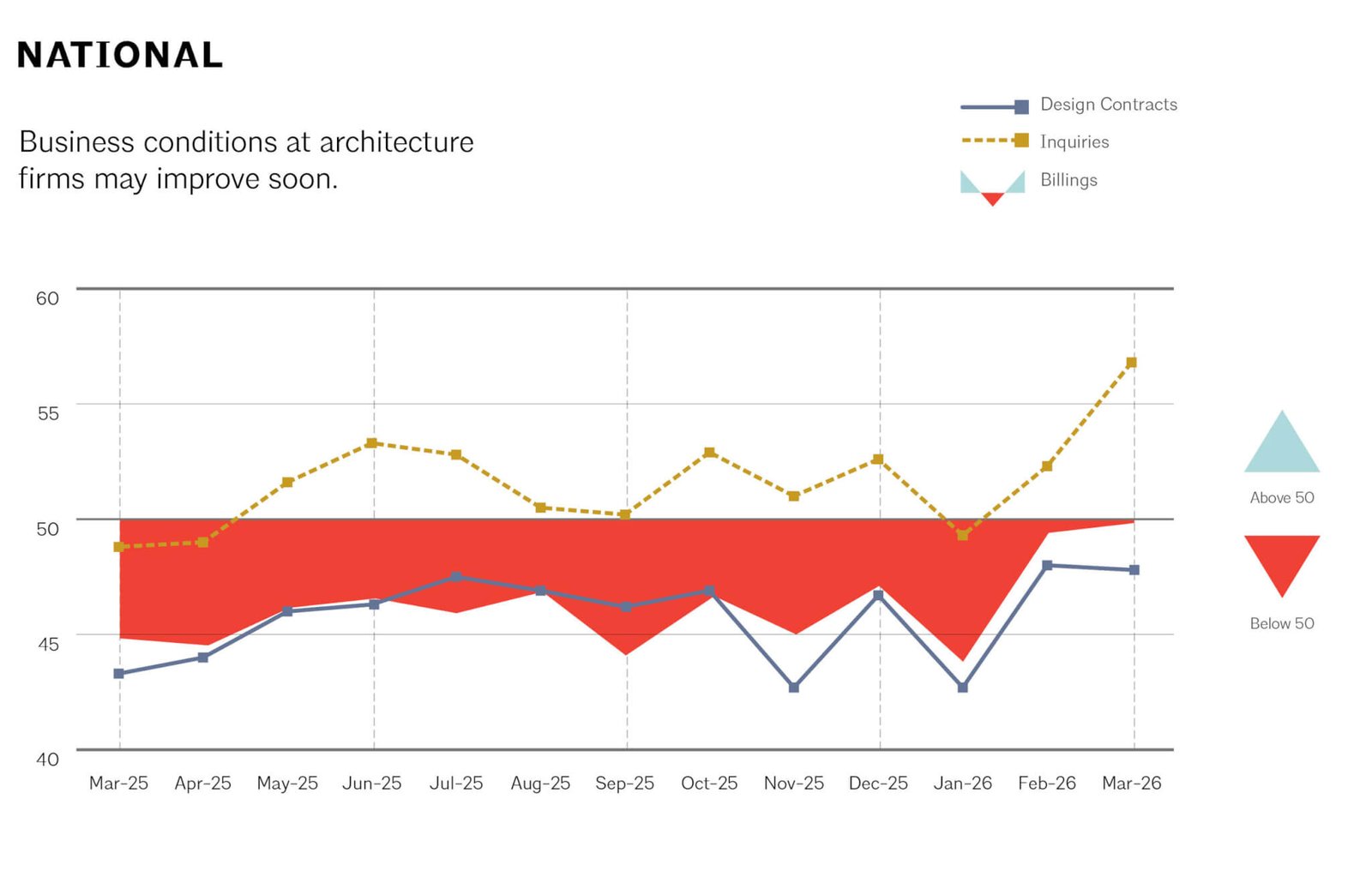

The AIA shared the Architecture Billings Index score for March this week: a strong-ish 49.8.

In its report AIA remarked that this is the closest the index has come to 50—any score above 50 indicates an increase in billings from the previous month—since early 2023 and with that the industry has reason for “cautious optimism.”

For comparison, in February the index fared relatively well too, reporting a 49.5, a notable jump from January’s 43.8. While billings at firms remain down overall, the March score indicates“near-equal shares of firms reporting increases and decreases.” On top of this, more good news is that new project inquiries have also increased, as indicated by the 56.8 index. The value of design contracts remains low and decreasing, however, with a score of 47.8.

A change from the sustained period of sluggish billings is a welcome one, however, AIA Chief Economist Richard Branch pointed out global conflicts have already affected the global economy and will likely continue.

“While billings could soon see positive growth for the first time in three years, ongoing economic and geopolitical challenges, such as the Iran conflict and labor shortages, pose significant risks to recovery,” Branch said in a statement. “These external issues will have a significant impact on the health of construction activity in both the near and long term.”

The AIA also noted that the project backlog at firms remains robust, averaging at 6.6 months.

In addition to the national average, the AIA also shared data on how each region of the country is faring. West reported a score of 50.6, constituting an increase in billings at respondent firms. Midwest is close behind with a score of 49.4. The Northeast continues to report decline in billings, as indicated by its low 44.2.

For this upcoming month if billings were to hold steady that would be a win, but with rising energy and oil prices and continued increases to inflation and the Consumer Price Index, “cautious optimism” is indeed the name of the game.